A Beginner’s Guide to Understanding Your Insurance Rates

August 11, 2022

We all know we are required to pay for home and auto insurance. However, do you know what goes into factoring those rates? How do insurance companies figure out what each insured will pay? Keep reading for our beginner’s guide on understanding your home and auto insurance costs.

Factors Used in Insurance Rating

There are many different factors used to determine how much you pay for your auto or home insurance. These factors can vary by the insurance company, your province, and the product you are insuring. With all these variables, it can be difficult to pinpoint how much you will pay without getting a quote from the company you are interested in.

First, many companies use their own loss experience to determine what to charge their customers. An individual’s risk profile matters to a great extent, certainly, but insurance carriers set their overall pricing on how profitable they are.

Additionally, there are some standard variables almost all insurance companies will use to base your price, so you can have a general idea of what will affect it. Because it can vary by the line of business, we will be looking at auto and home policies separately.

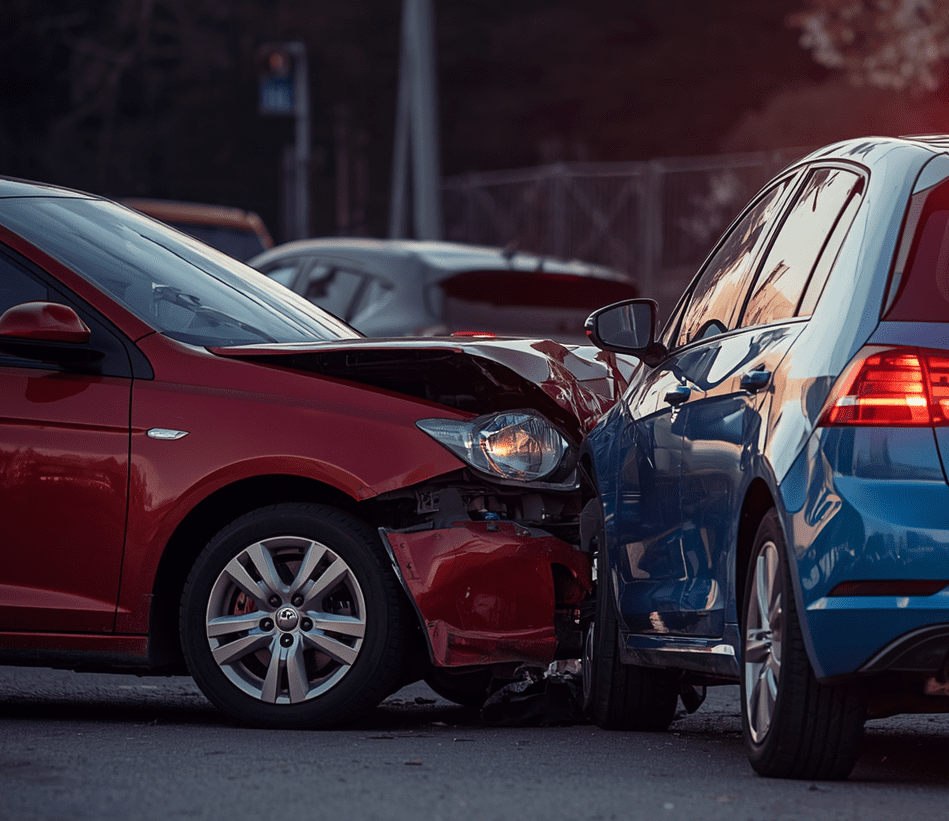

Auto Insurance

A common misconception is that the color of your car affects how much you will pay. However, that is not true. Regardless of the company, all insurance companies will base your price, at least in part, on what type of car you drive and your driving record. These factors can be directly linked to the risks they pose which help explain the price.

For example, a newer car with the latest technology will cost more to insure than an older one. This is because if this car were in an accident, it would cost more to repair or replace. As such, the insurance company will attempt to match the premium to this level of exposure.

The same goes for one’s driving history, the rates will be higher for someone who is a speeder or routinely gets into accidents. If you are a high-risk driver, you can expect to pay more in insurance. But of course, there is more to rating a car insurance policy than the type of car you have and your driving history.

The following are just some of the things insurance companies will look at to determine your price:

- Garage Address- Where your car is primarily stored overnight is essential as certain areas have higher rates of theft and vandalism. Pricing of your policy is based on which areas are statistically likely to have losses of these types and which are not.

- Insurance-Based Credit Score- It can be a hot topic, but many companies will use an insurance-based credit score to determine your likelihood of filing a claim. Typically, the higher your score, the better your price will be. While some aspects of a traditional credit score are used in the calculation, it is important to remember this is not the same as a credit score.

- Prior Insurance History- If you have had any prior lapses in coverage or have been canceled by a previous insurance company, you could be charged more for your insurance. Having too large of a gap between insurance policies or being canceled could indicate to insurance companies that you are not responsible and will file claims.

- Gender- Believe it or not, your gender also plays a part in the rating of your policy. Statistically, young males tend to be riskier to insure than females, and it is not uncommon for them to pay more to insure their cars.

- Marital Status- Marital status also comes into play. Much like younger males will cost more to insure, married males tend to be less risky, and their price will be lower as a result.

- Driving Experience- How long you have been driving is important as well. An inexperienced operator will pay more than someone who has been driving for decades so they have more experience being behind the wheel.

Home Insurance

Home insurance pricing is similar to auto insurance in that insurers will look at your location, insurance score, and loss history to get an idea of your price. But insurers base the price of your home insurance primarily on the home itself. Here are some factors used in pricing your home insurance premium:

- Age of Home- Older homes typically have older systems that can malfunction and cause losses, such as electrical, wiring, plumbing, or heating systems. Older homes may also have unique features and details that will cost more to replace than a newer home, which is another reason for the price difference. If you own an older home, you can typically expect to pay more for your insurance.

- Replacement Cost of Home- The amount it will cost to rebuild your home in a total loss plays a large part in how much you will pay for your insurance. It may seem obvious, but the more it will cost to rebuild your home, the more the price of your policy will be.

- Age of Roof- Similar to the age of your home, if you have an older roof, that can cause problems with leaks down the road. Because of this, many companies will base the price of your policy on how old your roof is. Homes with newer roofs will often pay less than those with older roofs.

- Proximity to Fire Station and Hydrant- While the location of your home matters when it comes to building costs, it is also imperative for insurers to know how close you are to the nearest fire station and fire hydrant. If you live within 5 miles of a fire station, the response time will be quicker if there were a fire. Therefore the damage to your home could be mitigated and you will pay less for insurance.

What Can You Do to Lower Your Price?

Knowing what insurance companies base your price on, you can work on things within your control to lower your premium. Here are some ideas on how to reduce the cost of your policies.

Improve Your Credit Score

Even though the insurance-based credit score is not the same as a credit score, it can be improved by increasing your credit score. Make sure your bills are paid on time and pay off any outstanding debts you may have. If your score increases, call your insurance company or agent to request a re-score of your policy.

Auto Telematics

If possible, look into enrolling in an auto telematics program that many companies are starting to offer as a basis for pricing. These programs utilize your driving data to determine how much of a risk you are on the road, which is either in the form of an app or a plug-in device for your car. Either way, it can potentially save you money if you are a safe driver. Some companies also include pay-per-use insurance, which bases your price on how much you drive.

Shop Around

You can save money on your home and auto insurance policies by shopping your rate at every renewal. Duliban Insurance Brokers are able to shop your policy with our 25 different insurance partners. Contact us for more information on saving on your auto and home insurance!