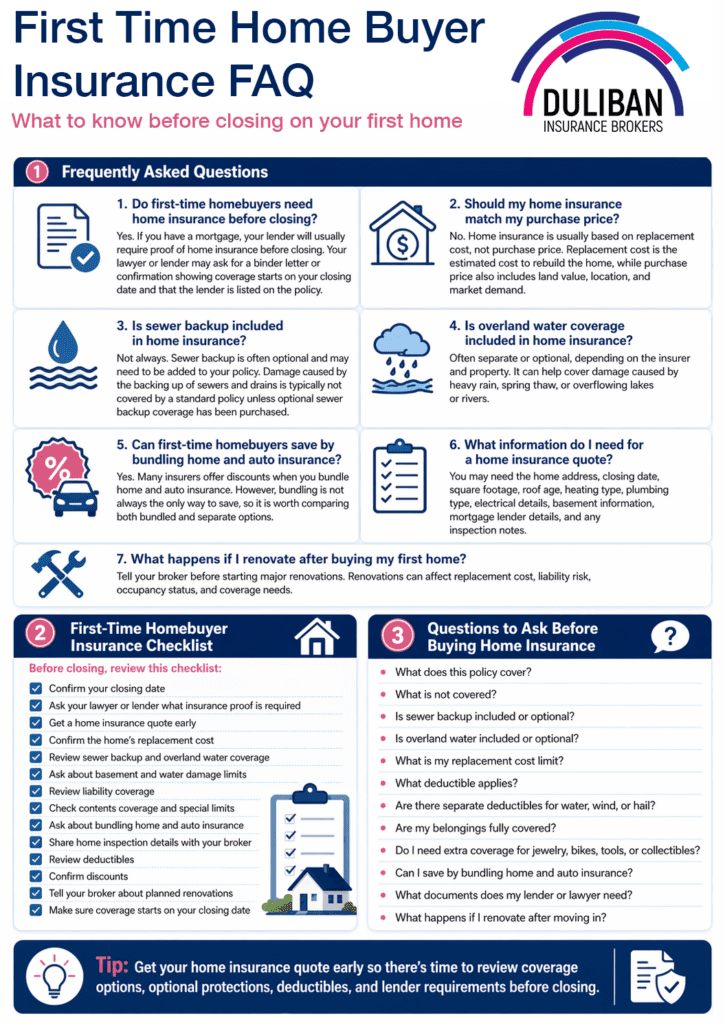

First-Time Homebuyer Insurance Tips in Ontario: What to Know Before Closing

Buying your first home is exciting, but it also comes with a long list of decisions. Between the mortgage, inspection, lawyer, closing costs, and moving plans, home insurance can feel like one more box to check.

But for first-time homebuyers in Ontario, home insurance is not something to rush through.

The right policy can help protect your house, your belongings, your finances, and your ability to recover after a loss. The wrong policy, or one chosen only because it was the cheapest, can leave you with coverage gaps you may not notice until it is too late.

Quick Answer: What insurance tips should first-time homebuyers know?

First-time homebuyers should make sure their home insurance is based on replacement cost, not purchase price. They should also review water damage coverage, sewer backup, overland water, liability limits, personal belongings, discounts, deductibles, and lender requirements before closing. In Ontario, it is also important to understand how the home’s age, roof, plumbing, electrical, heating system, and location can affect coverage and price.

A broker can help compare policies from multiple insurance companies and explain what is included, what is optional, and what may not be covered.

Do you need home insurance before closing?

Yes. If you have a mortgage, your lender will usually require proof of home insurance before closing. This is often provided through a binder letter or confirmation of insurance showing that coverage will begin on the closing date and that the lender is listed on the policy. Several real estate and mortgage resources note that proof of coverage is typically needed before closing so the transaction is not delayed.

This is why it is smart to start the insurance process as soon as your offer is accepted. Waiting until the last few days can create stress, especially if the insurer needs more details about the property.

Replacement cost is not the same as market value

One of the most common mistakes first-time homebuyers make is assuming their home insurance should match the price they paid for the house.

That is not how home insurance usually works.

Your home’s purchase price is based on market value. It includes factors like land value, location, demand, neighbourhood, lot size, and local real estate conditions.

Your insurance limit is usually based on replacement cost. This is the estimated cost to rebuild the home if it was damaged or destroyed. Replacement cost may include materials, labour, permits, demolition, debris removal, and construction costs.

For example, a home purchased for $650,000 may not cost exactly $650,000 to rebuild. It could cost more or less depending on the structure, finishes, location, and current construction costs.

This is why your broker or insurer may ask questions about:

- Square footage

- Age of the home

- Roof type and age

- Basement finish

- Exterior materials

- Heating system

- Plumbing type

- Electrical system

- Renovations or additions

- Detached structures, garages, or sheds

The goal is to insure the home properly, which can be more than just the mortgage amount or sale price.

The cheapest home insurance quote is not always the best choice

When buying your first home, it is natural to look for ways to save. You are already dealing with a down payment, land transfer tax, legal fees, moving costs, furniture, and maybe renovations.

But choosing home insurance only by price can be risky.

A lower premium may come with higher deductibles, lower limits, fewer optional coverages, or exclusions that matter for your home. For example, some water damage coverages may not be included automatically. Sewer backup and overland water coverage are often separate or optional coverages, depending on the insurer and property.

Before choosing a policy, ask:

- What is included?

- What is excluded?

- What coverage is optional?

- What deductible applies?

- Are there special limits on jewelry, bikes, tools, electronics, or collectibles?

- Is water damage coverage included, limited, or optional?

A good home insurance policy is not just about getting a low price. It is about knowing what you are actually protected for.

Water damage coverage deserves extra attention

For Ontario homeowners, water damage is one of the most important areas to review carefully.

Many first-time buyers assume that if water enters their home, their policy will automatically respond. That is not always true.

Some types of sudden and accidental water damage may be covered under a standard policy, but sewer backup, sump pump failure, and overland water may require specific coverage. Insurance Bureau of Canada notes that sewer backup is typically not covered by a standard policy unless optional sewer backup coverage has been purchased. It also describes overland water or flood coverage as protection for damage caused by heavy rain, spring thaw, or a lake or river overflowing.

First-time homebuyers should ask about:

- Sewer backup coverage

- Overland water coverage

- Sump pump failure

- Basement water damage

- Finished basement limits

- Water deductibles

- Exclusions for seepage or long-term leaks

- Backwater valve or sump pump discounts

This is especially important if the home has a finished basement, is near a body of water, is in a low-lying area, or has older drainage systems.

Your home insurance policy should protect more than just the building

Home insurance is not only about the physical house.

A typical home insurance policy may also include coverage for personal belongings, liability, additional living expenses, and detached structures, depending on the policy.

That means your policy may help protect:

- Furniture

- Clothing

- Electronics

- Appliances

- Tools

- Sports equipment

- Jewelry, subject to limits

- Personal liability

- Temporary living costs after an insured loss

- Garages, sheds, or other detached structures

Liability coverage is especially important. If someone is injured on your property, or if you accidentally cause damage to someone else’s property, liability coverage may help with legal or settlement costs.

This matters if you:

- Host guests

- Own a dog

- Have a pool

- Have a trampoline

- Rent part of your home

- Have a wood stove

- Have icy walkways in winter

- Plan to renovate

First-time buyers often focus on the house itself, but the liability side of home insurance can be just as important.

Your home inspection can help your insurance application

A home inspection is not only useful for understanding the condition of the home. It can also help your broker or insurer understand the property more accurately.

Insurance companies often look at the age and condition of major systems, including:

- Roof

- Furnace

- Plumbing

- Electrical

- Oil tank, if applicable

- Wood stove, if applicable

- Foundation

- Basement

- Water shut-off systems

- Sump pump or backwater valve

If the home has older wiring, outdated plumbing, an aging roof, or unique features, the insurer may ask for more details. In some cases, updates may be required before certain coverage is offered.

Sharing accurate inspection details early can help avoid surprises after closing.

When working with an insurance broker make sure you ask about discounts before you choose a policy

Many first-time buyers do not realize how many home insurance discounts may be available.

Depending on the insurer, you may qualify for savings if you:

- Bundle home and auto insurance

- Have a monitored alarm system

- Install a water leak detection system

- Have a mortgage-free home

- Are claims-free

- Pay annually instead of monthly

- Have newer roofing, plumbing, heating, or electrical systems

- Live near a fire hydrant or fire station

- Increase your deductible

- Belong to an eligible group or association

Bundling home and auto insurance is often one of the easiest ways to save, but it is not always the only option. A broker can compare both bundled and separate policies to see what makes the most sense for your situation.

Do not forget special limits on personal belongings on your home insurance policy

Most home insurance policies include contents coverage, but certain items may have special limits.

This can include:

- Jewelry

- Watches

- Bicycles

- Collectibles

- Fine art

- Musical instruments

- Tools

- Business equipment

- Sports equipment

- High-value electronics

If you own expensive items, ask whether they need to be scheduled or insured separately.

This is especially important for first-time buyers moving from an apartment or family home into their first property. You may be buying new furniture, appliances, electronics, or tools, and your contents value may be higher than you think.

What to consider for insurance when remodelling your first home

Many first-time homeowners plan updates after moving in. That could mean finishing a basement, replacing a kitchen, building a deck, adding a pool, upgrading electrical, or creating a home office.

Before starting renovations, contact your broker.

Renovations can affect your home insurance because they may change:

- The value of the home

- The rebuild cost

- The risk level

- Liability exposure

- Occupancy during construction

- Coverage for materials and tools

- Whether contractors need proof of insurance

Some renovations may require permits. Some may require updates to your policy. If you do not tell your insurer about major changes, it could create problems if you need to make a claim.

Why you should review your deductible before signing your insurance agreement

Your deductible is the amount you pay out of pocket before insurance responds to a claim.

A higher deductible may lower your premium, but it also means you take on more cost if something happens. A lower deductible may cost more each month, but it can make claims easier to manage financially.

First-time homebuyers should ask:

- What is the standard deductible?

- Are there separate deductibles for wind, hail, water, or sewer backup?

- How much would I pay out of pocket after a claim?

- Does increasing the deductible create meaningful savings?

- Am I comfortable paying that amount unexpectedly?

The cheapest premium is not always the best choice if the deductible is too high for your budget.

Why work with an insurance broker when buying your first home?

Buying your first home comes with enough pressure. Insurance should not be a last-minute scramble.

A broker can help you compare options, explain coverage differences, answer questions, and make sure the documents your lender or lawyer needs are ready for closing.

At Duliban Insurance, we work with a wide range of insurance providers, which gives first-time homebuyers more options when comparing price, coverage, and fit. Instead of guessing which policy is right, you can get advice based on your home, your budget, and your long-term plans.

First-Time Homebuyer Insurance Checklist

Before closing, review this checklist:

- Confirm your closing date

- Ask your lawyer or lender what insurance proof is required

- Get a home insurance quote early

- Confirm the home’s replacement cost

- Review sewer backup and overland water coverage

- Ask about basement and water damage limits

- Review liability coverage

- Check contents coverage and special limits

- Ask about bundling home and auto insurance

- Share home inspection details with your broker

- Review deductibles

- Confirm discounts

- Tell your broker about planned renovations

- Make sure coverage starts on your closing date

Questions to ask before buying home insurance

Before choosing a policy, ask your broker:

- What does this policy cover?

- What is not covered?

- Is sewer backup included or optional?

- Is overland water included or optional?

- What is my replacement cost limit?

- What deductible applies?

- Are there separate deductibles for water, wind, or hail?

- Are my belongings fully covered?

- Do I need extra coverage for jewelry, bikes, tools, or collectibles?

- Can I save by bundling home and auto insurance?

- What documents does my lender or lawyer need?

- What happens if I renovate after moving in?

Free First-Time Homebuyer Insurance Infographic

Duliban Insurance has created a free First-Time Homebuyer Insurance Infographic to help new buyers understand what to review before closing. The infographic explains important home insurance topics such as replacement cost, lender requirements, water damage coverage, sewer backup, overland water, liability protection, discounts, and common questions to ask before choosing a policy.

This resource is available to anyone who needs it, including first-time buyers, real estate agents, mortgage professionals, family members, and anyone preparing to purchase a home in Ontario.

Use the infographic as a simple reference before closing so you can better understand what home insurance protects, what may be optional, and what questions to ask before your policy begins.